.jpeg)

Kenya still talks about foreign exchange in the language of tea, tourism, horticulture and exports. The national imagination remains attached to the visible economy: the tea auction, the safari circuit, the flower farm, the port container, the visiting tourist. Yet the country’s most important hard-currency engine is increasingly invisible. It is a nurse in Dallas sending money to Kisii. A software engineer in London paying school fees in Eldoret. A construction worker in the Gulf supporting a family in Nyeri. A student in Australia topping up a parent’s M-Pesa wallet in Kakamega.

Diaspora remittances have crossed the $5 billion mark, placing them among Kenya’s most important sources of foreign exchange and making them more than a household-support mechanism. They sit at the centre of the country’s external stability, consumption, banking liquidity and fintech infrastructure. Kenya does not merely receive remittances. It runs part of its external stability through them.

The contradiction is that this lifeline remains expensive, fragmented and unevenly understood. The money is strategic, but the rails that deliver it still carry the scars of legacy finance: opaque foreign-exchange spreads, cash-heavy agent networks, bank intermediation, correspondent-banking costs, compliance burdens and uneven digital access. The result is a market that has become too important to remain treated as a side issue in diaspora policy.

That is why the question of who controls the remittance economy matters. This is no longer a small debate about money-transfer apps. It is a question about financial infrastructure, foreign-exchange liquidity, customer ownership, data, settlement rails and the future economics of cross-border payments.

This newsletter ranks the five most structurally important players in Kenya’s formal remittance economy: Safaricom PLC’s M-Pesa, Equity Bank Limited , Western Union , MoneyGram and KCB Bank Group. The ranking is not based on a single publicly disclosed market-share table, because no such complete table exists. It combines three practical measures: inflow capture, channel volume and structural importance. That means it deliberately mixes terminating wallets, bank channels and originating money-transfer operators, because that is how remittances actually move. A dollar sent from Seattle may begin with Remitly or Western Union, pass through a banking or settlement partner, and end in M-Pesa or an Equity account. The market is not a neat league table. It is a stack.

The macro picture: why $5 billion matters more than it looks

Kenya’s remittance market has moved from social support into macroeconomic relevance. Annual inflows are now roughly equivalent to 4–5% of GDP, with the United States remaining the dominant source corridor, followed by the United Kingdom, Gulf markets, Europe, Australia and other smaller corridors. North America remains the anchor of the system, while the Gulf has become more volatile because its flows are tied to labour-market rules, employment conditions, taxation and migration policy in host economies.

The policy significance is straightforward. Remittances are not debt. They do not require Eurobond refinancing. They do not arrive through an IMF programme. They are private transfers, but their aggregate effect is public. They support household consumption, increase foreign-exchange supply, help stabilise the shilling, fund education and healthcare, and create deposit flows that banks can turn into credit. They are also more distributed than export earnings. Tea receipts are concentrated in a value chain. Tourism dollars are tied to hotels, airlines and parks. Remittances land directly in millions of households.

The problem is cost. Sub-Saharan Africa remains one of the most expensive regions in the world for sending money, and Kenya is not exempt from that burden. The average cost of sending $200 into the country remains well above the UN Sustainable Development Goal target of 3%, although the actual price varies sharply by corridor, provider and channel. Some digital routes are already far cheaper. Cash-heavy, card-funded and bank-mediated channels can remain far more expensive once transfer fees and foreign-exchange margins are included.

On a $5 billion annual market, every percentage point saved returns roughly $50 million to households. Closing the gap between high-cost channels and the 3% target could keep hundreds of millions of dollars inside Kenya’s household economy. Put differently, remittance costs are not merely a consumer-protection issue. They are a macroeconomic leakage. When fees, FX spreads and avoidable settlement friction take hundreds of millions of dollars out of the system, that is not just inconvenience. It is household income diverted into the machinery of legacy finance.

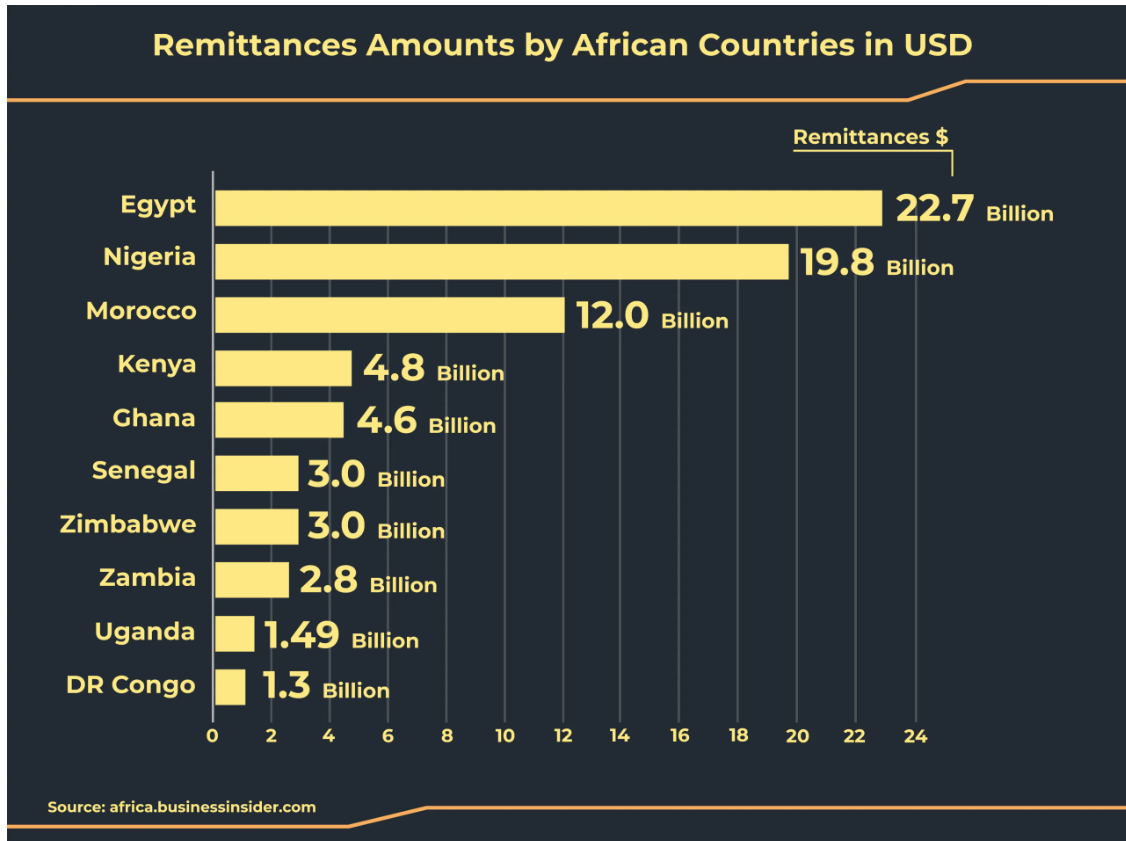

The continental comparison sharpens the point. In Egypt, remittances are not just household transfers but one of the country’s most important foreign-exchange pillars, helping to steady reserves and cushion an economy often under pressure from import bills and currency stress. In Nigeria, they play a similar role, though in a much larger and more volatile economy, where diaspora inflows help support household consumption, supplement FX supply and partly offset the fragility of oil dependence. In Morocco, the story is more deeply institutionalised: decades-old migration ties to France, Spain and Italy have made remittances a durable balance-of-payments support, woven into household welfare, housing demand and domestic liquidity. Kenya ranks below all three not because remittances matter less, but because the top tier benefits from larger diaspora populations, older migration corridors and, in Morocco’s case especially, more mature formal remittance channels. What Kenya does have is a more digital receiving architecture, which means its opportunity may lie less in matching their scale immediately and more in extracting more value from every dollar that already arrives.

Who controls the flow?

The five dominant players each control a different layer of the remittance machine. M-Pesa is the dominant receiving wallet and last-mile rail. Equity Bank is the most visible diaspora-banking platform and one of the most important bank-channel aggregators. Western Union and MoneyGram still matter because legacy money-transfer operators retain large parts of the originating and cash-based transfer market. KCB Bank completes the group because of its balance sheet, branch network, MTO partnerships, regional banking footprint and wholesale settlement relevance.

That ranking leaves out several important challengers, including Wise, Remitly, WorldRemit, Sendwave (International Remittance), LemFi , NALA, Taptap Send, Chipper Cash and Wapi Pay PTE LTD. That omission is not a dismissal. It reflects the difference between dominance today and disruption tomorrow. The digital challengers are eating into fees, improving customer experience and reshaping corridor economics. But based on publicly visible information, most do not yet have independently verifiable Kenya-specific volume large enough to displace the five infrastructure players.

Kenya’s remittance market cannot be understood by looking only at the brand the sender sees on an app, or the wallet where the recipient finally receives the money. A single transfer may involve an originating fintech, a compliance layer, an FX provider, a settlement bank, a local payout partner, M-Pesa, a bank account, an agent network or a cash-out point. Value is captured at different stages, and power sits in different places depending on the corridor, customer type and payout method. This is why the market looks fragmented from the outside but highly structured once the flows are traced end to end. Remittances are not one business. They are a chain of businesses sharing one transaction.

1. Safaricom M-Pesa: the irreplaceable terminus.

M-Pesa is the most important institution in Kenya’s remittance economy because it is where a large share of remittances end. Market estimates differ on the exact share, with some references placing M-Pesa’s role around half of formal remittance inflows and others suggesting a higher figure when wallet termination is included. The safest formulation is this: M-Pesa is the dominant terminating wallet for inbound remittances into Kenya, and nearly every major remittance provider must integrate with it, directly or indirectly, to reach Kenyan households at scale.

Its advantages are structural. M-Pesa has tens of millions of active users, deep agent density, instant domestic settlement and a trust position that most banks and fintechs cannot easily replicate. For a sender abroad, the logic is simple. The recipient already has M-Pesa. The phone number is the account. The user experience is familiar. The money can be spent, withdrawn, saved, used to pay bills or moved into adjacent products.

Its weakness is also structural. M-Pesa is both infrastructure and competitor. Every money-transfer operator that pays into M-Pesa strengthens Safaricom’s last-mile power, but M-Pesa Global also competes with those same players in outbound and cross-border flows. That creates a platform tension familiar to every digital economy: the marketplace owner also sells products on the marketplace.

Safaricom’s advantage is not simply mobile money. It is distribution, identity, data, liquidity and habit. Any fintech that wants to reach Kenyan households must decide whether to partner with M-Pesa, compete with it, or build around it. For now, partnership remains the rational answer.

2. Equity Bank: the diaspora-banking platform.

Equity Bank’s role in the remittance market is different from M-Pesa’s. It is not trying to be the universal last-mile wallet. Its stronger play is what happens once diaspora money enters the formal banking system. Over the years, Equity has built one of Kenya’s clearest diaspora-banking propositions, linking remittance receipt to accounts, mortgages, savings products, construction finance, investment services and dedicated diaspora support.

That makes Equity less of a pure remittance channel and more of a relationship platform. Its market position is best understood through bank-channel depth, partner networks and cross-sell potential rather than a simple claim of total remittance share. In a market where many transfers end as consumption, Equity’s opportunity is to turn a portion of those flows into deposits, credit histories, housing finance and long-term financial relationships.

Its advantage is cross-sell. A pure remittance app earns from the transaction. A bank can earn from the relationship. Once money lands in an Equity account, it can become a deposit, a mortgage repayment, a construction loan, an investment account or working capital for a family business. That is why Equity’s diaspora strategy should be seen as a balance-sheet strategy, not merely a remittance strategy.

That weakness appears long before the money reaches Kenya. The sender in Boston is usually opening Remitly, Wise, Sendwave or LemFi, not an Equity interface. That is where the rate is compared, the fee is judged and the habit is formed. By the time the funds land in Nairobi, Equity is often the receiving bank rather than the brand the customer remembers choosing. It can book the deposit and earn from the balance, but the first moment of trust, convenience and loyalty may already belong to someone else. In remittances, the institution that receives the money is not always the one that owns the relationship.

For Equity, the strategic task is to make the receiving account matter after the money lands. A remittance that arrives into an Equity account should not remain a one-off family transfer. It should become the basis for a savings record, a construction loan, a mortgage conversation, an investment product or working capital for a household business. That is where the bank can defend its role against lower-cost apps: not by trying to out-app Remitly or Wise at the sending end, but by turning the money received in Kenya into a fuller financial relationship.

3. Western Union: the eroding incumbent.

Western Union remains a giant because trust and physical distribution still matter. It has the brand recognition of an institution that shaped global money transfer long before fintech was a word. In Kenya, its relevance comes through bank partnerships, agent networks, cash-pickup corridors and direct-to-wallet integration. It remains especially important for older, cash-preferring, first-generation and less digitally confident users.

Its advantage is resilience. Western Union has survived regulatory tightening, fintech competition, mobile money and declining cash usage because it has compliance infrastructure, liquidity, a global agent network and deep brand memory. For many families, Western Union is still the name that means “money has arrived.”

Its disadvantage is the legacy cost base. Cash networks are expensive. Agent commissions, compliance costs, FX spreads and older settlement systems all add friction. Digital pricing has compressed in some US-Kenya use cases, but cash-heavy channels can remain materially more expensive once fees and FX margins are included. Western Union is not uniformly expensive in every channel, but its legacy cash model is structurally more exposed than digital-first alternatives. Western Union is not simply a company to dismiss. It is a warning about moats. Distribution is powerful until customer behaviour changes. Once users trust apps, wallets and transparent FX pricing, the physical-agent moat begins to shrink.

4. MoneyGram: the private-equity reinvention

MoneyGram occupies a similar but slightly different position. It is smaller than Western Union but still deeply relevant in Kenya through bank distribution, mobile-wallet termination and long-standing international corridors. Its Kenya footprint includes bank and mobile-money integrations that keep it embedded in formal remittance flows, even as digital challengers attack its margins.

Its advantage is flexibility. As a private company, MoneyGram can modernise without the same quarterly-market pressure faced by listed firms. It has also experimented with digital channels and stablecoin settlement, giving it a potentially stronger reinvention story than many observers assume. In a world where settlement rails are changing, MoneyGram’s willingness to test new infrastructure matters.

Its disadvantage is strategic compression. It faces Western Union on brand, M-Pesa on last-mile ubiquity, banks on trust and fintechs on price. That is an uncomfortable middle position. MoneyGram must become more digital without losing cash users, more transparent without giving up margin, and more innovative without weakening the compliance confidence that keeps regulators and banking partners comfortable.

MoneyGram represents the classic incumbent dilemma. The company has assets, licences, relationships and brand trust. But the profit pool is moving away from visible fees and toward FX, settlement, data, customer ownership and embedded financial services.

5. KCB Bank: the broad-distribution challenger.

KCB’s case is less obvious to the casual reader, which is why it matters. KCB is not ranked because it is the loudest diaspora brand. It is ranked because it has the balance sheet, branch network, corporate relationships, regional footprint and partner integrations that matter in bank-channel and wholesale flows. Its role in settlement, correspondent flows and integration with rail providers such as TerraPay, Thunes and Onafriq gives it relevance beyond ordinary retail remittance receipt.

Its advantage is institutional depth. KCB can serve retail recipients, corporate importers, regional businesses and high-value transfers. Its position in East Africa gives it an advantage where remittances intersect with trade, intra-African flows and SME liquidity.

Its disadvantage is visibility. Equity owns the diaspora-banking narrative more effectively. M-Pesa owns the consumer wallet. Digital fintechs own the low-cost app experience. KCB’s role is real, but harder to communicate. That makes it strategically important but editorially less obvious.

KCB is the reminder that not all infrastructure is consumer-facing. Some of the most important players in remittances sit behind the scenes: settlement banks, liquidity providers, compliance gateways and wholesale rails.

The challengers: who is eating the incumbents.

The challenger layer deserves attention because it is changing customer expectations even where it has not yet displaced the dominant infrastructure players. Wise, Remitly, WorldRemit, Sendwave, LemFi, NALA, Taptap Send, Chipper Cash and WapiPay are reshaping the market through pricing transparency, faster onboarding, direct-to-wallet payout, corridor-specific marketing and cleaner digital experiences.

Wise represents transparency. Its promise is arithmetic. The sender sees the fee, the rate and the amount to be received. Remitly represents corridor-focused digital scale, particularly in large diaspora markets where speed and convenience matter. WorldRemit and Sendwave represent mobile-first African payout, with M-Pesa and other wallets forming the last mile. LemFi and NALA represent diaspora-native fintech, built around African users who want low-cost, app-based transfers without the friction of legacy providers. WapiPay represents a different kind of specialisation: Asia-Africa and trade-linked settlement rather than the heavily contested US-Kenya and UK-Kenya consumer remittance corridors.

WapiPay’s strategic importance is about corridor specialisation. The company has reported meaningful transaction volumes, but publicly available data does not yet allow a firm independent ranking against Kenya’s dominant remittance channels. Its real distinction lies in Asia-Africa and trade-linked settlement, a space still underserved compared with the crowded US-Kenya and UK-Kenya consumer corridors.

The broader point is not that one challenger will immediately topple M-Pesa, Equity, Western Union, MoneyGram or KCB. The point is that challengers are resetting the price ceiling and the experience standard. Once a user has seen transparent FX pricing, instant wallet delivery and a simple app interface, the patience for opaque fees declines.

Where the margin is moving.

The Kenya remittance value chain is splitting into three layers.

The first is the customer-facing layer: apps, brands, fees, speed, user experience and trust. This is where Wise, Remitly, Sendwave, LemFi and Western Union’s digital products compete most visibly. The customer-facing layer gets the headlines because it is what users see. It is also the layer where price comparison is easiest and loyalty is most fragile.

The second is the termination layer: wallets, bank accounts, cash-out points and local liquidity. This is where M-Pesa, Equity and KCB matter most. The money may originate through a slick app abroad, but it must still land somewhere trusted in Kenya. That endpoint determines whether the transfer becomes cash, consumption, savings, a loan repayment, merchant payment or business capital.

The third is the settlement layer: correspondent banking, FX liquidity, stablecoins, wholesale rails, APIs, compliance infrastructure and real-time payment links. This is where TerraPay, Thunes, Onafriq, Stellar, Circle-style stablecoin rails and bank treasury desks begin to matter. Most consumers will never see this layer, but it is where the economics of the market may change most dramatically.

The old market made money from opacity. The new market will make money from control points: owning the customer, owning the wallet, owning the bank relationship, owning the settlement rail or owning the compliance gateway. The squeezed middle is the legacy retail MTO that owns neither the cheapest rail nor the deepest customer relationship.

The regulatory architecture: why the rules still shape the winners

Kenya’s remittance market is becoming more digital, but regulation still determines who gets to compete, who gets to partner, and who gets to scale. The Central Bank of Kenya’s Money Remittance Regulations created the formal licensing path for money remittance providers, but the real barrier is no longer just minimum capital. It is operational trust: anti-money laundering controls, know-your-customer systems, Financial Reporting Centre reporting, segregated customer accounts, fit-and-proper director tests, bank partnerships and the ability to satisfy correspondent-banking scrutiny.

That is why banks retain a structural advantage. Equity, KCB, Co-operative Bank, NCBA and other regulated banks do not approach remittances as narrow transfer businesses. They sit inside the financial system already. They have balance sheets, compliance teams, branch networks, treasury functions and existing relationships with regulators. A fintech may win the customer interface, but a bank can still sit behind the transaction as settlement partner, liquidity provider, account holder or trust anchor.

Foreign fintechs increasingly enter Kenya through partnerships with locally licensed entities, banks or payment infrastructure providers. That model lowers market-entry friction, but it also turns licensing into a commercial asset. The licence holder becomes more than a compliance box. It becomes a gatekeeper into the Kenyan remittance economy. For smaller players, the burden is heavier. Kenya’s continued exposure to enhanced AML scrutiny and correspondent-banking caution raises the cost of doing business, especially for firms without deep compliance infrastructure.

This is the quiet protection enjoyed by incumbents. It is not always written as protection. It appears as due diligence, settlement access, risk scoring, bank onboarding, audit requirements and compliance costs. The policy challenge is to preserve financial integrity without freezing competition. If regulation only rewards the biggest and most established players, remittance costs will fall more slowly than technology allows.

The global lesson: cheaper rails are already being built elsewhere.

Kenya does not need to imagine what a lower-cost remittance future looks like. Other markets are already testing parts of it.

India has used its domestic payments strength as an exportable financial infrastructure story. The country’s UPI system has become a reference point for how real-time payment rails can lower cost, improve visibility and support bilateral payment links. The lesson for Kenya is not that UPI can be copied wholesale. It is that national payment infrastructure becomes more powerful when it is designed for interoperability beyond the domestic market.

The Philippines offers a different lesson. Its remittance economy has long been treated as national infrastructure because overseas Filipino workers are central to the country’s external account. Wallets such as GCash have become more than consumer apps. They are channels for savings, credit, merchant payments, insurance, international receipt and diaspora-linked financial services. The remittance does not end when money arrives. It becomes the first step into a wider financial ecosystem.

Mexico is the most disruptive precedent. Stablecoin-enabled settlement has begun to show how cross-border value can move faster and at lower cost when dollar liquidity, blockchain rails and local real-time payment systems are combined. The consumer may still see a familiar app or WhatsApp interface, but the back end is changing. Money can move through stablecoin rails, convert locally, and settle into domestic payment systems at a lower cost than traditional correspondent banking allows.

Kenya should pay attention because it has many of the ingredients these markets use separately. It has one of the world’s most sophisticated mobile-money ecosystems. It has a large and committed diaspora. It has strong bank distribution. It has a growing fintech sector. It has regulators that understand systemic payments better than many peers. What it still lacks is a fully coordinated remittance strategy that treats cost reduction, interoperability, FX liquidity, consumer protection and diaspora investment as one agenda.

Stablecoins, diaspora bonds and the next policy frontier.

The next phase of remittances will not be decided only at the consumer-app layer. It will be shaped at the settlement layer. Stablecoins are likely to arrive first as wholesale infrastructure rather than as mass-market remittance brands. A sender may still use a familiar app. A recipient may still receive shillings into M-Pesa or a bank account. But between those two points, the economics of settlement could change materially if regulated stablecoin rails reduce dependence on slower and more expensive correspondent-banking chains.

Kenya’s emerging virtual-asset regulatory framework gives policymakers a chance to shape this transition before it becomes informal. The key question is not whether stablecoins will touch remittances. They already do in many corridors globally. The question is whether Kenya will allow them into the formal system under clear reserve, licensing, disclosure, consumer-protection and AML standards. A controlled framework could lower wholesale settlement costs, support faster payout, improve transparency and create new roles for licensed Kenyan institutions as on-ramps, off-ramps, liquidity managers and compliance gateways.

Diaspora bonds are the other missing piece. Kenya has often spoken about mobilising diaspora capital, but remittance flows remain largely consumption-led and under-structured from an investment perspective. That is not a criticism of households. Families send money first for the needs in front of them: food, school fees, rent, medical bills, land, housing and small businesses. The policy question is how to create credible, trusted and liquid instruments that allow diaspora money to support national development without forcing families to choose between household obligations and investment.

Pakistan’s Roshan Digital Account offers one useful reference point. Its success came from making diaspora participation easy, digital, yield-bearing and linked to formal financial products. Kenya does not need to copy the model exactly. It needs the same seriousness of execution. A diaspora bond that is delayed, poorly communicated or distributed through clunky channels will struggle. A diaspora product embedded into trusted wallets, banks and investment platforms, with transparent pricing and credible guarantees, would stand a better chance. Remittances are already financing Kenya informally. The country now needs better instruments to retain more value, convert more flows into productive capital, and lower the cost of moving money home.

What this means for Kenya

Remittances in Kenya do more than top up household budgets. They underpin reserves, credit, consumption and regional liquidity. Most remittances land in M-Pesa wallets or bank accounts and are either spent locally or recycled into the financial system. That means they move quickly from private support into school fees, rent, healthcare, construction materials, retail purchases, merchant payments and deposits.

Every percentage point reduction in remittance costs translates almost directly into additional household income retained in Kenya. If annual remittances are about $5 billion, a one-point reduction keeps roughly $50 million in the hands of senders and recipients. A five-point reduction would be worth roughly $250 million. Converted into shillings, that becomes material purchasing power across towns, villages, schools, hospitals, shops and small businesses.

This is why cheaper remittances should be treated as financial inclusion, not just payments efficiency. A lower-cost corridor is effectively a private-sector subsidy to households, except that no Treasury allocation is required. It boosts rural purchasing power, democratizes access to foreign currency and injects liquidity into regions that may not benefit directly from export earnings or formal wage growth.

For Kenya, the opportunity is not only to receive more remittances. It is to retain more value from the remittances already arriving.

What changes from here.

Three forces are likely to reshape Kenya’s remittance market over the next two years.

The first is the shift from cash-funded transfers to account-funded digital channels. Any policy or pricing change that makes cash transfers more expensive will accelerate migration toward bank accounts, cards, wallets and digital-first remittance apps. That favours Wise, Remitly, Sendwave, LemFi and bank-linked channels. It puts pressure on Western Union and MoneyGram’s traditional retail base, even if both incumbents remain important in cash-heavy and trust-sensitive corridors.

The second is the arrival of stablecoin-enabled settlement. This will not immediately replace M-Pesa, banks or money-transfer operators. More likely, it will sit behind them. The consumer interface may remain unchanged while the settlement economics underneath compress. That creates opportunity for licensed remittance providers, banks, payment aggregators and infrastructure fintechs that can operate compliant on/off-ramps between dollar stablecoins and Kenyan shillings.

The third is M-Pesa’s evolution from passive terminus to active cross-border competitor. For years, many providers needed M-Pesa because it was the best way to reach Kenyan households. That remains true. But M-Pesa Global changes the posture. Safaricom is not only receiving the market. It is increasingly competing for outbound, intra-African and cross-border flows. That makes its role more powerful, but also more sensitive from a competition and regulatory perspective.

The five dominant players will likely remain central through the near term, but the economics around them are shifting. Safaricom’s position as the leading terminating wallet remains structurally strong. Equity’s diaspora-banking flywheel is durable, but it must defend the customer relationship against lower-cost apps at the sending end. Western Union and MoneyGram are not disappearing, but their strongest position is narrowing toward cash-heavy, trust-sensitive and less-digitised corridors. KCB’s wholesale and settlement relevance could become more valuable as the infrastructure layer becomes more important. The fintech challengers will collectively gain share, but the market is still more likely to fragment than to crown a single new winner.

What now?

For banks, remittances should be treated as an acquisition channel, not a back-office flow. Equity has understood this better than most. KCB has the balance sheet to do more. Co-operative Bank, NCBA, I&M, Absa and Stanbic should think less about receiving transfers and more about converting remittance behaviour into savings, mortgages, SME credit, investment accounts, insurance and diaspora wealth products.

For fintechs, the opportunity is not just cheaper transfers. The next frontier is remittance-linked credit scoring, compliance-as-a-service, diaspora merchant payments, SME import settlement, predictable FX tools and embedded savings. Competing on zero fees alone is a weak long-term strategy unless the business model captures value elsewhere.

For telecoms, M-Pesa’s dominance is both a privilege and a regulatory exposure. Safaricom should continue expanding cross-border functionality, but it must also manage the perception that every remittance provider is paying rent to the same unavoidable rail. Airtel Money has room to position itself as the credible alternative termination wallet, especially if it can build stronger remittance partnerships.

For regulators, the priority should be transparent pricing, open access, proportionate licensing and safe innovation. CBK and related agencies should push clearer disclosure of total remittance cost, including FX margin, while supporting responsible experimentation in real-time settlement, stablecoins, diaspora-linked financial products and lower-cost corridors. The goal should not be to pick winners. It should be to make extraction harder and competition easier.

For investors, the market is bigger than consumer apps. The more durable opportunity may sit in infrastructure: liquidity management, compliance tooling, payout aggregation, FX optimisation, wallet interoperability, stablecoin settlement, diaspora credit and cross-border SME payments. The best companies may not look like remittance brands. They may look like rails.

The verdict

Kenya’s remittance economy has outgrown the way the country talks about it. This is not simply money sent home by relatives abroad. It is a distributed foreign-exchange system, a household-stability engine, a banking acquisition channel, a telecom monetisation layer and a fintech battleground.

The five dominant players each control a different part of the machine. Safaricom controls the most important last-mile wallet. Equity controls the most developed diaspora-banking proposition. Western Union and MoneyGram still control trust, cash access and global origination in key corridors. KCB controls institutional depth, regional balance-sheet strength and wholesale relevance. Around them, digital challengers are forcing the market to become faster, cheaper and more transparent.

The next phase will be decided by who owns the rails, who owns the customer, who controls liquidity, who satisfies regulators, and who can turn a remittance into a broader financial relationship.

Kenya cannot wait for cheaper remittances to emerge accidentally from global competition. The mathematics is too large and the stakes are too direct. Every shilling saved in transfer costs is a shilling that stays in Kenya’s economy.

Kenya does not merely receive remittances. It runs part of its external stability through them. The companies that move those dollars are no longer service providers at the edge of the economy. They are becoming part of the country’s financial infrastructure.